What Is A Home Mortgage All About?

Article by-Ramirez LundGetting a home mortgage can be a tricky process for people because they have no idea what is required in order to get approved. Anyone can improve their chances by reading reading quality tips about home mortgages such as the one's in the following article. Read on and get educated in the field of home mortgages.

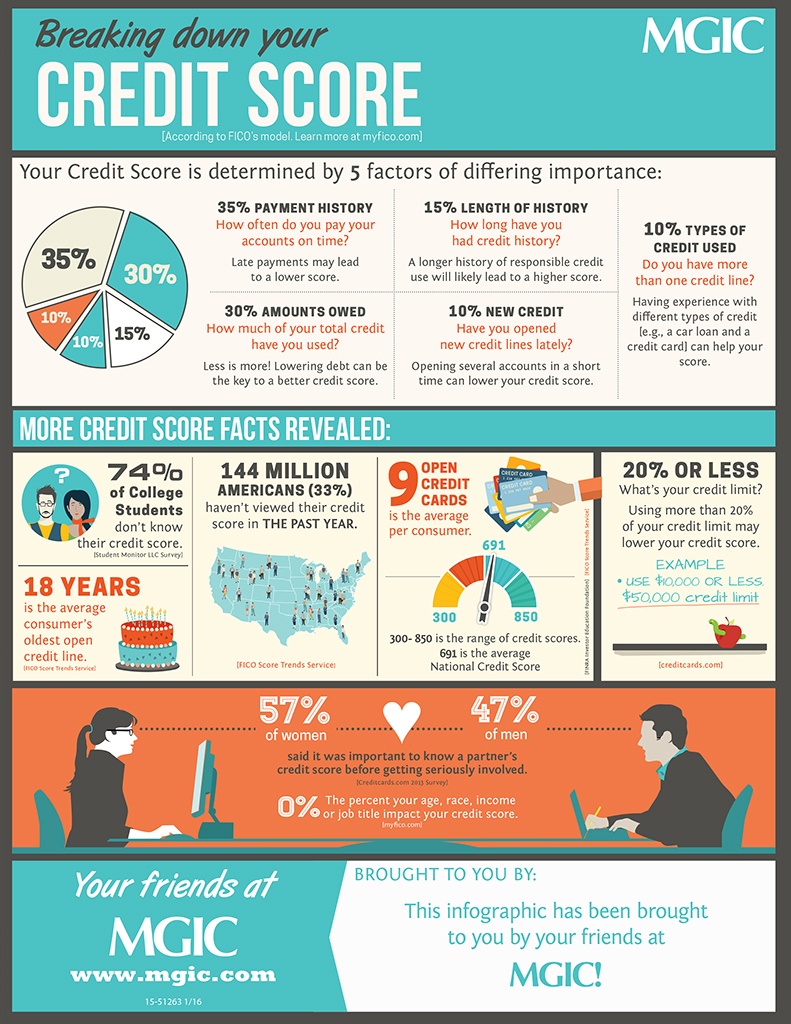

Before trying to get a mortgage approval, find out your credit score. Mortgage lenders can deny a loan when the borrower has a low credit score caused by late payments and other negative credit history. If your credit score is too low to qualify for a mortgage loan, clean up your credit, fix any inaccuracies and make all your payments on time.

Do not waste time in your home mortgage process. After you've submitted a mortgage application to the lender, this is when your clock start ticking. You have to send any necessary documents for the application process quickly. Any delays could destroy a purchase and cost you your deposit. Get an expected closing date, and then keep in touch with the lender periodically until your loan closes. Some lenders close quicker than others.

Try getting pre-approved for your mortgage. It helps you know what you're able to spend before you bid on properties. It also helps you avoid getting attached to a home that is out of your price range. The process is generally simple: you contact a mortgage lender, submit the personal and financial information, and then wait for their response. Some information in this process will include the amount you can afford and your loan's interest rate. You will receive a pre-approval letter from your lender, and then you'll have the funds as soon as the seller accepts the bid. Your pre-approval process may not be this simple, but it could be.

Reducing your debt as much as possible will increase your chances of being approved for a mortgage. If you are not in a good financial situation, meet with a debt consolidation professional to get out of debt as quickly as possible. You do not need to have a zero balance on your credit cards to get a mortgage but being deeply in debt is definitely a red flag.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

Try going with a short-term loan. Since interest rates have been around rock bottom lately, short-term loans tend to be more affordable for many borrowers. Anyone with a 30-year mortgage that has a 6% interest rate or higher could possibly refinance into a 15-year or 20-year loan while still keeping their the monthly payments near around what they're already paying. This is an option to consider even if you have slightly higher monthly payments. It can help you pay off the mortgage quicker.

When you decide to apply for a mortgage, make sure you shop around. Before deciding on the best option for you, get estimates from three different mortgage brokers and banks. Although, interest rates are important, there are other things you should consider also such as closing costs, points and types of loans.

If you've gotten approved for a mortgage, don't make any other big purchases until after you've closed on your home. Typically your lender will pull your credit once again right before closing. If there are issues that crop up it could lead to problems with your closing. Be smart and curb spending until all is complete.

If your appraisal isn't enough, try again. If the one your lender receives is not enough to back your mortgage loan, and you think they're mistaken, you can try another lender. You cannot order another appraisal or pick the appraiser the lender uses, however, you may dispute the first one or go to a different lender. While the appraisal value of the home shouldn't vary drastically too much between different appraisers, it can. If you think the first appraiser is incorrect, try another lender with, hopefully, a better appraiser.

Know your mortgage interest rate type. When you are obtaining home financing you should understand how the interest is calculated. Your rate could be fixed or it could be adjustable. With fixed interest rates, your payment will usually not change. Adjustable rates vary depending on the flow of the market and are variable.

If you have bad credit, avoid applying for a home mortgage. Although you may feel financially ready enough to handle the costs of a mortgage, you will not qualify for a good interest rate. This means you will end up paying a lot more over the life of your loan.

Before you contact a mortgage lender to apply for a loan to buy a home, use one of the fast and easy mortgage calculators available online. You can enter your loan amount, the interest rate and the length of the loan. The calculator will figure the monthly payment that you can expect.

Avoid interest only type loans. With an interest only loan, the borrower only pays for the interest on the loan and the principal never decreases. This type of loan may seem like a wise choice; however, at the end of the loan a balloon payment is needed. This payment is the entire principal of the loan.

Make sure that you compare mortgage rates from several companies before you settle on one. Even if the difference seems to be minimal, this can add up over the years. One point higher can mean thousands of extra you will have to shell out over the course of the loan.

Be sure to gather all your financial documentation and have it ready in a single file before applying for a home mortgage. You will need to have bank statements, tax returns, W2 forms and pay stubs on hand. Some lenders require additional documentation of income and responsibility. Be sure to find out what is needed before applying.

https://www.forbes.com/sites/francoisbotha/2021/02/22/the-google-generation-of-family-offices-how-these-40-banks-are-preparing/ can save money on a mortgage by going with a lender who offers to finance with no closing costs. Closing costs are a significant part of a mortgage. To make up for that lost money, however, the lenders will make up it in some other way. Usually with a slightly higher interest rate.

Be sure that you know exactly how long your home mortgage contract will require you to wait before it allows you to refinance. Some contracts will let you within on year, while others may not allow it before five years pass. What you can tolerate depends on many factors, so be sure to keep this tip in mind.

As you can see, there's a lot you don't know about the home mortgage business. Using https://bankingjournal.aba.com/2021/10/the-evolving-regulatory-landscape-of-esg/ like the ones listed above can help you to not only locate a loan but they can also ensure that you find a low-interest loan that won't leave you playing catch-up on a month-to-month basis. So always seek out information before acting.